I'm going to take next week off for time with friends and family. See you in 2007. And as a little holiday treat. Here's a link , from Tim Minahan, to the value of sourcing. It seems that e-sourcing will save you 80% on the cost of the 12 days of Xmas.

Cheers,

David Rotor

Friday, December 22, 2006

Wednesday, December 20, 2006

Engaging internal clients

In Buying Market Share I touched on the idea of measuring procurement department effectiveness through the share a category manager has earned (compliance) of the internal market to purchase their good or service as well as the share of an internal client's overall spend that the procurement department has earned. To improve, the procurement department needs to better meet the needs of its market. The simplest way to do this is to understand the market, whether it is for a single category across the organization, or the multi-category spend of an internal business unit.

stolen from borrowing on skills and techniques from the sales world that allows the procurement team to engage with their clients in order to better understand their requirements and drive improved market share. For readers with experience in strategic sourcing, this level of engaging with a client is similar to what is done during a category sourcing exercise, but moves from being a event driven exercise to embedding it as a recurring procurement department business process. Here’s a graphic that provides a summary of the Client Engagement process.

Monday, December 18, 2006

Buying market share

There are a few topics that routinely get discussed in the procurement world. Later today I'll be talking with some ex-colleagues about a situation where their client wants a deeper understanding of how success will be measured in an outsourced procurement environment. Tim Minahan, at The Aberdeen Group, was thinking about this topic recently as well. Tim is an old hand at procurement services, and is one of the more reliable commentators for this sector. Here's a comment I left in response to his KPI post.

Hi Tim,

I agree with your comment:

“No single metric defines supply management success. (Although, I personally believe that spend under management, as defined above, comes pretty darn close.)”

I’ve been using “spend under management” as the leading indicator (metric) for indirect procurement department effectiveness for several years now. I’ve found it effective across several industries, and even in the public sector. I also often refer to it as our department’s “market share” as executives in other business units understand the language, and often intuitively accept that market share growth is “good”.

I measure procurement market share against two axis. First, from a category manager’s perspective, what’s the corporate-wide compliance with each of our category offerings. For example, “the compliance rate for our preferred cell phone carrier was 89% last quarter”. The second axis is from a customer perspective; what’s our market share for a given client department. For example, “our market share of the COO’s spend is 92%”.

The value of this approach is it provides feedback to allow the procurement department to understand what the rest of the organization values, and what it does not. It also enables discussions around client requirements “why is our market share so low on the east coast?”

Cheers,

David Rotor

Thursday, December 14, 2006

Bending over backwards when you're buying

When you're trying to create a strategy to lower the category cost of a good or service within for a company it's practically a given that among the first things that is done is to attempt to aggregate demand for a particular good or service. There is the usual tussle between centralizing control and delegating authority out to regions or business units. It's probably no surprise that I tend to come down on the central control side of the argument when it comes to procurement, but what may surprise some is that I attribute less of the value to centralization to aggregated volume than I do to access to information. Experience has proven to me that buyers armed with lots of recent market knowledge routinely will negotiate better deals than buyers armed only with bigger volumes. This post will try to provide a partial justification for that opinion, and it's based on a couple of special cases of supply and demand curves from our friends in economics, the backward bending supply curve and the u-shaped cost curves. I've used material from Wikipedia to help illustrate my points.

Standard supply and demand theory tries to explain how the amount of demand for a good or service and the amount of supply of that good or service interact. In relation to the amount of supply, the more demand there is for something, the higher the market price. The more supply there is in relation to the demand the lower the market price. Here's an illustration from the wikipedia entry.

This is the primary reason why buyers like to aggregate their demand - assuming adequacy of supply the more you buy (the red downward sloping line) the lower your per unit costs should be. Of course, in the real world sales teams don't pay much attention demand curves and will happily charge companies with larger volumes higher prices.

The backward bending demand curve is often used to describe labour markets "As a person's wage increases, they are willing to supply a greater number of hours working, but when the wage reaches an extremely high amount (say a wage of $4,000 per hour), the amount of labor supplied actually decreases". I can't recall ever seeing this behaviour in the market, or at least that couldn't more accurately be described as simply lowering supply and increasing price. It is worth having buyers understand, if only to help them understand that the standard curves don't always apply.

The u shaped cost curve, where the cost of a good or service initially decreases with volume and then begins to increase with additional volume is pretty common in real markets. There are many reasons, the main reason why companies accept a supplier having a u shaped cost curve is that the increased price they pay to a supplier that has a higher cost with more volume is often lower than the company would incur for introducing a new supplier "switching costs". The u shaped cost curve looks like this (don't blame wikipedia for this one).

I've run into this curve several times, usually while negotiating corporate-wide, or nation-wide deals for companies. Here are a few examples:

I've run into this curve several times, usually while negotiating corporate-wide, or nation-wide deals for companies. Here are a few examples:

With time, expertise, and the ability to test the market frequently, buyers can get a reasonable level of understanding of when a price curve for a good or service will begin to curve upwards. Often it is a function of both volume and geographic dispersion. It might cost a supplier more to service one city than another depending on how much business they have in each location. You might find that a supplier has production capacity constraints that you are bumping up against.

You want your buyers to lower the total cost of a category of good or service. They should consciously be aggregating and disaggregating volume to find the optimal "demand" offer to the market. That often means letting them pay a premium for a given geography or range of goods and services if that means an aggregate lower cost overall.

Cheers,

David Rotor

Standard supply and demand theory tries to explain how the amount of demand for a good or service and the amount of supply of that good or service interact. In relation to the amount of supply, the more demand there is for something, the higher the market price. The more supply there is in relation to the demand the lower the market price. Here's an illustration from the wikipedia entry.

This is the primary reason why buyers like to aggregate their demand - assuming adequacy of supply the more you buy (the red downward sloping line) the lower your per unit costs should be. Of course, in the real world sales teams don't pay much attention demand curves and will happily charge companies with larger volumes higher prices.

The backward bending demand curve is often used to describe labour markets "As a person's wage increases, they are willing to supply a greater number of hours working, but when the wage reaches an extremely high amount (say a wage of $4,000 per hour), the amount of labor supplied actually decreases". I can't recall ever seeing this behaviour in the market, or at least that couldn't more accurately be described as simply lowering supply and increasing price. It is worth having buyers understand, if only to help them understand that the standard curves don't always apply.

The u shaped cost curve, where the cost of a good or service initially decreases with volume and then begins to increase with additional volume is pretty common in real markets. There are many reasons, the main reason why companies accept a supplier having a u shaped cost curve is that the increased price they pay to a supplier that has a higher cost with more volume is often lower than the company would incur for introducing a new supplier "switching costs". The u shaped cost curve looks like this (don't blame wikipedia for this one).

I've run into this curve several times, usually while negotiating corporate-wide, or nation-wide deals for companies. Here are a few examples:

I've run into this curve several times, usually while negotiating corporate-wide, or nation-wide deals for companies. Here are a few examples:- Waste removal for a US based national housing REIT

- Travel agency and card services for a global telecommunication firm

- PCs for a national Canadian bank

- Office supplies for a national government

- Airline travel for a global media company

- Facility Management services for a commercial property REIT

- MRO and parts for a military

- Engineering supplies for a continental freight railway

- Food and snacks for a global media company

- Consulting services for a national government

- Packaging supplies for a global manufacturer

- Consumer shopping bags for a national retailer

- Recycling services for a brand-name retailer

With time, expertise, and the ability to test the market frequently, buyers can get a reasonable level of understanding of when a price curve for a good or service will begin to curve upwards. Often it is a function of both volume and geographic dispersion. It might cost a supplier more to service one city than another depending on how much business they have in each location. You might find that a supplier has production capacity constraints that you are bumping up against.

You want your buyers to lower the total cost of a category of good or service. They should consciously be aggregating and disaggregating volume to find the optimal "demand" offer to the market. That often means letting them pay a premium for a given geography or range of goods and services if that means an aggregate lower cost overall.

Cheers,

David Rotor

Tuesday, December 12, 2006

Shipping Costs - not quite a Marginal Revolution

Tyler Cowen over at Marginal Revolution, posted a suggestion to read this article at the New York Times. The author, Meline Toumani, makes the point that sea containers, the "giant metal boxes" have had a dramatic impact on the viability of trading goods internationally. One point I disagree with is her quote - The process is so efficient that transport costs have become "little more than a footnote in a company’s cost analysis" from author Mark Levinson's book “The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger”. She goes on to attribute Macy's decision to source clothes in Malaysia rather than down the block largely to a reduction in shipping costs. Having done strategic sourcing work for Macy's and its sister firms in the Federated Department Stores family, I can't quite agree. Labour rate arbitrage has, to my mind, more to do with the cost advantage Malaysia has over the garment district.

Let's take a look at Levinson's comment. PricewaterhouseCoopers,(1) published "Cutting your distribution cost" in 2004. Here's a chart from the report, that shows that distribution costs remain substantially more than a footnote:

The data, which seems pretty representative from the companies I've looked at, shows that transportations costs ranged from 0.27% to 12.57% with a median of 2.15% expressed as a percentage of revenue. I can tell you that Macy's isn't at the low end of the range, and few companies would consider even 27 basis points of their revenue as a footnote.

In another client situation, a hospital organization in the US North East. They spent about $750M annually, with just under $4M of that going for freight and logistics. When we took a look at the $4M in spend, they had over 2,000 suppliers providing transportation services. Savings in this one category were on the order of $500K. While, perhaps, not the most important spend category for every firm, I'd take a hard look at them when you're trying to reduce your costs for goods and services.

Cheers,

David Rotor

(1) - Under "full disclosure", I previously worked for PricewaterhouseCoopers, as a Vice President of Global Sourcing.

Let's take a look at Levinson's comment. PricewaterhouseCoopers,(1) published "Cutting your distribution cost" in 2004. Here's a chart from the report, that shows that distribution costs remain substantially more than a footnote:

The data, which seems pretty representative from the companies I've looked at, shows that transportations costs ranged from 0.27% to 12.57% with a median of 2.15% expressed as a percentage of revenue. I can tell you that Macy's isn't at the low end of the range, and few companies would consider even 27 basis points of their revenue as a footnote.

In another client situation, a hospital organization in the US North East. They spent about $750M annually, with just under $4M of that going for freight and logistics. When we took a look at the $4M in spend, they had over 2,000 suppliers providing transportation services. Savings in this one category were on the order of $500K. While, perhaps, not the most important spend category for every firm, I'd take a hard look at them when you're trying to reduce your costs for goods and services.

Cheers,

David Rotor

(1) - Under "full disclosure", I previously worked for PricewaterhouseCoopers, as a Vice President of Global Sourcing.

Monday, December 11, 2006

Food bank economics

I listened to a "feel good" news story this morning on CBC where the station was congratulating itself on raising funds for a local food bank. The bit that really caught my attention was that the food bank is better off with cash donations than food item donations; they have negotiated wholesale prices from food distributors.

Good for them, a local non-profit community service organzation is using their market power to lower their operating costs, and improve the volume of goods they can deliver to their clientele. It left me wondering though; here's my line of thought.

First, as I understand it, food banks mostly serve "working poor", people with jobs or who are on some form of fixed income, who are not earning enough to meet their basic needs. Second, there is usually some form of rationing, such as one food hamper per family per week. Assuming for a moment these two assumptions are true, I wonder whether the food banks can extend their discounted prices to their clients? Their clients are presumably paying for some of their own food, at retail pricing, only getting a partial subsidy from their periodic free hampers. By extending the preferential pricing to their clients they would be able to further their organization's goals, and may in fact, also add to their market power, increasing their ability to negotiate preferential pricing for food.

Good for them, a local non-profit community service organzation is using their market power to lower their operating costs, and improve the volume of goods they can deliver to their clientele. It left me wondering though; here's my line of thought.

First, as I understand it, food banks mostly serve "working poor", people with jobs or who are on some form of fixed income, who are not earning enough to meet their basic needs. Second, there is usually some form of rationing, such as one food hamper per family per week. Assuming for a moment these two assumptions are true, I wonder whether the food banks can extend their discounted prices to their clients? Their clients are presumably paying for some of their own food, at retail pricing, only getting a partial subsidy from their periodic free hampers. By extending the preferential pricing to their clients they would be able to further their organization's goals, and may in fact, also add to their market power, increasing their ability to negotiate preferential pricing for food.

Friday, December 8, 2006

Outsourcing business cases

I'm spending some time thinking through an outsourcing business case. The client has an expectation that the proposal will fit into their existing budget for the function (procurement and payables), independent legacy systems will be retired and new functionality will be added with the introduction of an integrated system, and ideally costs will be lowered. On the other side the service provider understandably wants to do all that, and turn a reasonable profit. So far, so good.

The difficulty is that the service provider's business case is turning up at about 150% of the existing budget. The work can be pretty quickly broken down into three areas to explore, plus one more:

The existing budget

This is a classic outsourcing issue, service provider's routinely strive to identify expand what's included in the existing budget, and client's routinely try to limit what's included. Direct costs are reasonably straight forward to nail down, allocated indirect costs such as contributions for space, corporate technology, support functions such as HR and accounting, are the usual areas that cause conflicts, and can determine whether a deal proceeds or fails.

The service provider's cost model

This tends to be a great area for "pursuit teams" (sales) to delve into in great depth. Most large outsourcing service providers have built wonderfully complex cost models to help them capture what it will cost to service an account. Routinely, I'll find that there is a bit of a fortress mentally around the cost model and it can often be as difficult to get the team to disclose line item details from the cost model as it is to get the client to share detailed budget information.

The first area to explore is whether the costs are market based or internally derived - don't accept the assertion from the cost team that they are market based, go and test the market yourself.

The second area to test is whether the internal costs have been inflated with an internal mark-up, again the cost team will routinely suggest they do not mark up costs, prove it for yourself.

The third area to examine are the overheads, are there too many people loaded onto the deal, are there costs loaded such as standard space or technology charges for people that have already had those costs modelled as direct costs for the contract, etc.

Going back over the last decade I've seen numerous cases where the cost team has contributed to proposals being, literally hundreds of millions of dollars over the market.

The service provider's pricing model

There is often little a pursuit team can do about the margin the company wants to earn from a contract, you win or lose in the market and margins will be adjusted to reflect that reality. What the pursuit team can do is vigorously target the "risk" model that can increase or decrease the margin calculation. Most (likely all) the major outsourcing service providers have developed formal risk management frameworks in their internal deal approval process. The one for the deal I'm looking at now runs about 200 questions, such as: Is the proposed deal a "factory" deal or a "fortress" deal? “Factory” means that it can be managed in a shared service facility, “fortress” means it is a unique offering that is customized for the client. Fortress deals have, in the model, a higher risk factor, and the discount rate applied to the price model is increased. Each of the 200 or so questions have similar impact on the discount rate. The pursuit teams need to spend time understanding the risk model, but often it is viewed as an administrative exercise, and the pursuit team doesn't ever really understand how the model will impact the success or failure of their proposal.

Strategic Sourcing

Outsourcing teams should also consider lowering the cost of goods and services in the function they are taking over by using strategic sourcing. I won't get into it in this post, but it's often possible to lower those costs by 10% or more, enough that many deals will live or die on the application of sourcing to the deal. Spending time to have an expenditure analysis performed to determine if there is an opportunity is well worth considering.

Cheers,

David Rotor

Thursday, December 7, 2006

Phil Nimmons speaks

Another quick post that has little to do with procurement. As I mentioned on Tuesday, I was in Toronto for a couple of meetings and to attend a concert at the CBC's Glen Gould Theatre by the Dave McMurdo Jazz Orchestra. The concert was recorded, and will air February 25, 2006 on CBC's "OnStage". The feature of the evening was the Canadian premiere of Phil Nimmon's "Conversations (Aural Communication)", a piece Phil wrote last year as the inaugral "SOCAN/IAJE Phil Nimmons Established Composer Award". Conversations is classic Nimmons, it's all instrumental and showcases several of the great soloists in Dave's band. It's not the most accessible style of Jazz, without a vocalist to guide the audience instrumental jazz tends to require active attention.

Throughout the piece I could hear Phil's desire to have the piece represent the musicans and their instruments talk to each other. I found it was like a really successful party where there are a bunch of interesting people chatting to each other with sometimes one and sometimes several conversation threads happening at once. One of the highlight soloist bits was Alex Dean on sax doing a bit of "free-blowing". I don't know if it was intentional but it sure seemed to be a homage to the way Phil is best known for playing, just this side of out of control, arms, legs, and body practically bouncing off the stage. Elaine and I and a few friends thoroughly enjoyed seeing the band live again, getting 20 people on stage playing live jazz doesn't happen very often in Canada.

Throughout the piece I could hear Phil's desire to have the piece represent the musicans and their instruments talk to each other. I found it was like a really successful party where there are a bunch of interesting people chatting to each other with sometimes one and sometimes several conversation threads happening at once. One of the highlight soloist bits was Alex Dean on sax doing a bit of "free-blowing". I don't know if it was intentional but it sure seemed to be a homage to the way Phil is best known for playing, just this side of out of control, arms, legs, and body practically bouncing off the stage. Elaine and I and a few friends thoroughly enjoyed seeing the band live again, getting 20 people on stage playing live jazz doesn't happen very often in Canada.

Tuesday, December 5, 2006

Auditory consumption

Short post today - I'm off to Toronto for a concert and will squeeze a couple of business meetings in too.

Monday, December 4, 2006

Dell in the news

The Economist has an article, Commoditize This, about Dell. In summary, it points out that Dell faces some challenges, it has lost its market leader status in PCs to HP, there are some regulatory investigations going on, and its market focus, direct sales to businesses, is growing slower than HP's retail to consumer business. Michael Dell is placing a bet on growing his services business, but the Economist rightly points out that the growth of IT service businesses in India may make that move less profitable than Dell would like. I used to be a big supporter of Dell when acquiring a "fleet" of desktop and laptop PCs for clients. The market has moved on, but Dell used to have a significant cost advantage over IBM and the rest of the firms competing in the business PC market, and they used that advantage to sell more PCs than anyone else. The standard analysis was that Dell's model of build-to-order and direct ship to customer was their cost advantage driver. Several teams I had take a look at this market for global firms all came to the same conclusion; a bigger advantage came from Dell's repair and warranty supply chain.

Standard practice, in many industries not just PC assemblers, is to develop highly analytical models using meantime to failure and other factors to determine how many of which parts are going to be needed to support the repair and warranty requirements for a product. The manfacturer will then run a production run to stock inventory to support this expected consumption. The Dell model changed the PC industry, what Dell realized was that the fleet of PCs they sold were themselves a supply chain of inventory for the repair and warranty business. They developed better models than their competitors, largely based on cannibalizing returned and broken PCs for good parts. The cost advantage from this model began at over 10% and slowly declined over several years.

Standard practice, in many industries not just PC assemblers, is to develop highly analytical models using meantime to failure and other factors to determine how many of which parts are going to be needed to support the repair and warranty requirements for a product. The manfacturer will then run a production run to stock inventory to support this expected consumption. The Dell model changed the PC industry, what Dell realized was that the fleet of PCs they sold were themselves a supply chain of inventory for the repair and warranty business. They developed better models than their competitors, largely based on cannibalizing returned and broken PCs for good parts. The cost advantage from this model began at over 10% and slowly declined over several years.

Friday, December 1, 2006

Buying a cell phone this season? You may want to wait until March.

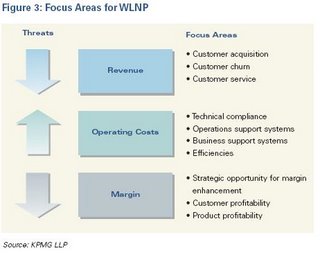

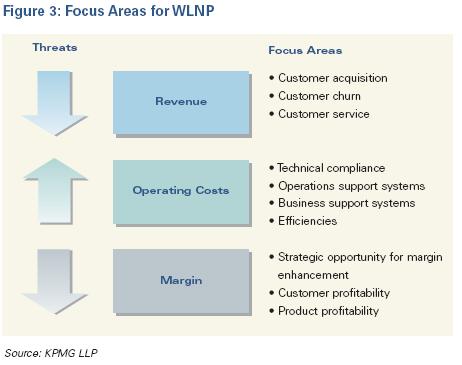

If you're a Canadian and in the market for a new cell phone contract (for yourself or for your company) you should consider that wireless number portability (WLNP) is coming to Canada next March. WNLP is old news in much of Europe, Asia, and of course the US. WLNP allows a cell-phone subscriber to keep their cell-phone number when they switch service providers. For consumers it removes one of the main disincentives to switching. Few people enjoy the hassle of informing friends, family, and colleagues that they have a new cell-phone number, its probably even more disruptive than changing a home phone number as the industry doesn't have the equivalent of "411" service to find a contact's new number. Experience in the US, the UK, and many other countries shows that WLNP increases competition and decreases consumer cost. KPMG, the consulting firm, wrote a whitepaper on WLNP during the transition in the US. They identifed three major factors that will impact cell carriers; declining revenue, increasing operating costs, and declining margins.

As a consumer you won't have much opportunity to personally influence these factors, but you should see the market impact of WLNP very quickly come March. I would recommend holding off on signing up for a new multi-year wireless contract until the impact is reflected in the market. Corporate buyers should think about not only waiting for the market impact of WLNP, but also what they can do to influence the focus areas that KPMG identifies for each factor. A couple of obvious areas are to lower the cost to service your account, such as moving to web-based reporting and eliminating mailed statements. Can you allow the carrier to sell premium services or hardware directly to your employees? As always, understanding the seller's issues "market knowledge" is key to negotiating the best deal for your company.

As a consumer you won't have much opportunity to personally influence these factors, but you should see the market impact of WLNP very quickly come March. I would recommend holding off on signing up for a new multi-year wireless contract until the impact is reflected in the market. Corporate buyers should think about not only waiting for the market impact of WLNP, but also what they can do to influence the focus areas that KPMG identifies for each factor. A couple of obvious areas are to lower the cost to service your account, such as moving to web-based reporting and eliminating mailed statements. Can you allow the carrier to sell premium services or hardware directly to your employees? As always, understanding the seller's issues "market knowledge" is key to negotiating the best deal for your company.

Subscribe to:

Comments (Atom)

{kind=link}